Trends

Let's cut through the fintech noise.

Every year, some analyst calls fintech "the most disrupted industry on the planet," and every year the same four companies still control your mortgage, your credit card, and your savings account. But something is genuinely different heading into 2026.

The infrastructure of money itself is being rewired — not by startups pitching to venture capitalists, but by regulators forcing open data access, central banks issuing programmable currency, and AI agents that can actually execute financial decisions without a human in the loop.

So here's what actually matters, backed by hard numbers from the CFPB, McKinsey, Accenture, the Federal Reserve, and other organizations that measure what's really moving — not what's trending on LinkedIn.

Top fintech trends going into 2026:

Let's get into it.

The biggest shift in financial services right now isn't a new product. It's a new category of actor. AI agents don't just recommend financial decisions — they execute them.

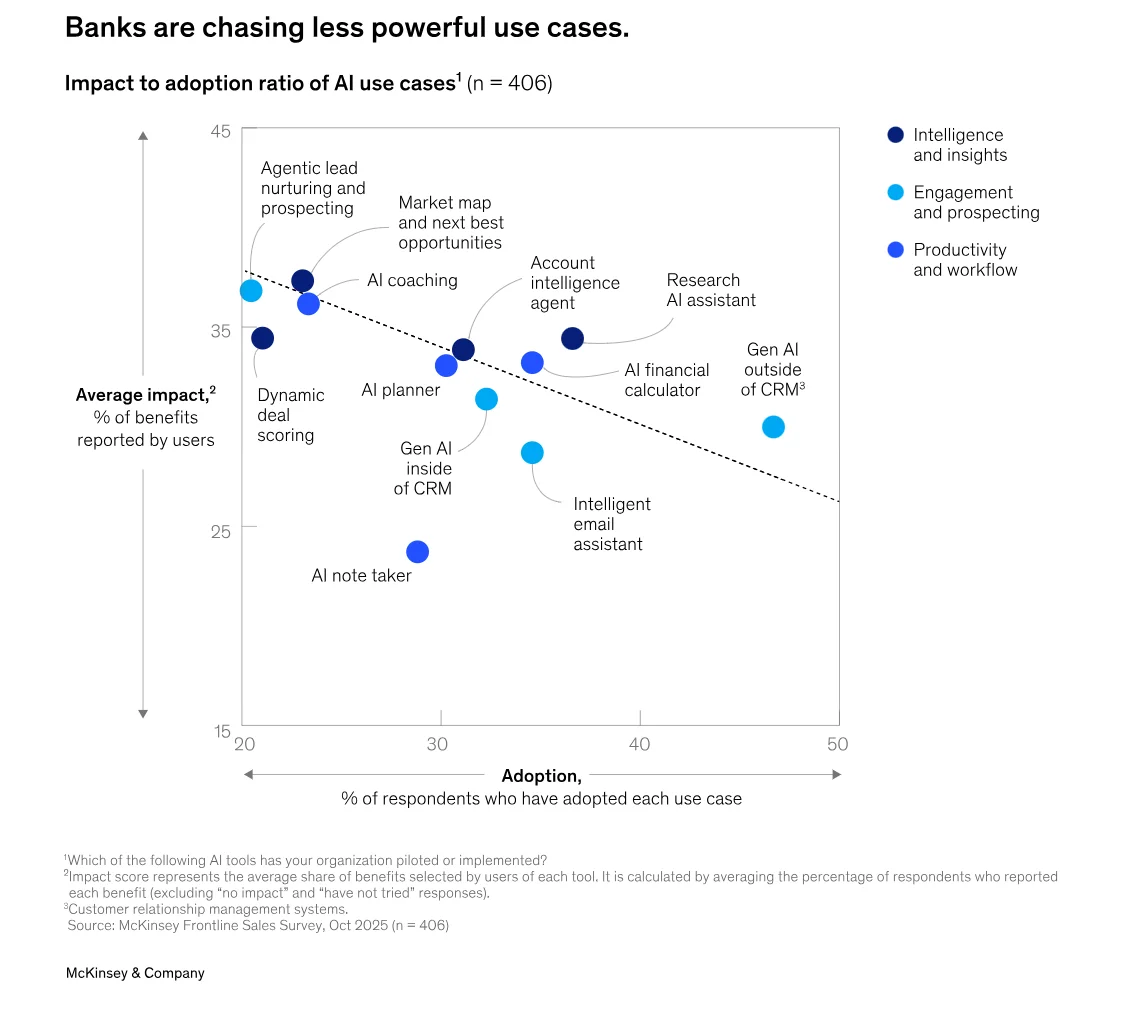

The transition to 'Agentic Banking' is no longer speculative. According to Accenture’s 2026 Banking Outlook, the top 200 global banks stand to capture $289 billion in value from scaled AI adoption. This shift is reflected in executive sentiment: while 88% of leaders are increasing budgets for agentic capabilities, the real story lies in the specialized ROI. CEO-sponsored programs in the sector are outperforming peers with 2.5x higher returns, largely driven by a 20% reduction in net costs (McKinsey) and a massive acceleration in back-office functions like financial forecasting.

In financial services, this means AI that can autonomously negotiate loan terms, rebalance portfolios in real-time, dispute fraudulent charges, switch insurance providers, and execute trades — all within defined guardrails, without human intervention.

While general enterprise adoption of agentic AI sits at 62%, in financial services — an industry with enormous volumes of repetitive, rules-based work — the penetration rate is even higher. According to the McKinsey 2025 Frontline Sales Survey, over 60% of banking professionals have already been using AI in their daily workflows for at least six months.

In high-volume areas like corporate credit, this shift is moving beyond experimentation toward a 'multi-agentic' model that McKinsey estimates could deliver a 40% to 80% productivity uplift per use case. 61% of financial institutions are now using cloud-based AI orchestration to move from passive Copilots to autonomous agents that handle over 45% of routine knowledge work in initial pilots.

JPMorgan Chase has evolved beyond its legacy COiN (Contract Intelligence) platform — which once famously cut 360,000 hours of manual contract review — into a pioneer of "Agentic Commerce." In 2026, the firm is deploying autonomous AI agents that don't just flag risks but use delegated authority and advanced reasoning to execute transactions and manage "always-on" treasury functions.

Salesforce launched Agentforce for Financial Services, enabling autonomous AI agents that handle customer onboarding, KYC document collection, loan status updates, and claims processing — executing multi-step workflows end-to-end across their financial services CRM.

Goldman Sachs has shifted from basic search tools to a "hybrid workforce" model, deploying agentic AI like Devin across its 12,000-person engineering team to autonomously manage code migration and debugging. The firm is integrating these agents into core operations—such as transaction reconciliation and client onboarding — achieving 3x to 4x productivity boosts. In this case, AI operates as a digital employee executing complex, multi-step tasks rather than just retrieving information.

Gartner predicted that 40% of enterprise applications would feature task-specific AI agents by 2026 — up from less than 5% in 2025 — and that inflection is now underway. In financial services, the battleground is "financial action layers" — APIs purpose-built for AI agents to do things with money, not just analyze it.

Banks that expose clean, permissioned action APIs will attract the developers building the next generation of autonomous finance tools. Those that don't will be disintermediated by those that do. (For a broader look at how agentic AI is reshaping enterprise operations across every industry, see our generative AI trends for 2026.)

The most structurally significant fintech event of the past decade didn’t emerge from a Silicon Valley garage; it was codified in Washington, D.C.

In October 2024, the Consumer Financial Protection Bureau (CFPB) finalized the Personal Financial Data Rights rule under Section 1033 of the Dodd-Frank Act. This wasn't just another compliance hurdle—it was a declaration of independence. By requiring financial institutions to share consumer data with authorized third parties at the consumer’s request — securely and at no cost — the CFPB effectively ended the era of data hoarding.

Translation: your bank no longer owns your financial data. You do.

For years, the fintech ecosystem survived on the fragile practice of screen-scraping — a clunky, insecure workaround that banks frequently blocked. Section 1033 replaces this "digital duct tape" with a federal mandate for standardized, API-based pathways.

As we move through 2026, we are seeing the "Open Banking ROI" materialize in real-time. According to McKinsey's Global Banking Annual Review, open banking participants see 2-3x higher product cross-sell rates and 40% lower customer acquisition costs compared to traditional banking models. In Europe, where open banking under PSD2 has been live since 2019, the market has already demonstrated what happens when you give consumers data portability.

The structural impact is also drawing massive capital. Research from the National Bureau of Economic Research found that following open banking mandates, venture capital investment in the sector typically doubles. This surge occurs as the competitive "moat" shifts from the mere possession of data to the ability to build superior services on top of it.

With the implementation timeline currently moving through mid-sized and community banks, the playing field is leveling, ensuring that service quality — not data ownership — determines the market winners.

Plaid — the infrastructure layer connecting 8,000+ financial apps to 12,000+ financial institutions — processed over 13 billion consumer-permissioned transactions in 2024. Their network now represents the backbone of open finance in the US, and Section 1033 legally secures access that was previously dependent on goodwill and screen-scraping workarounds.

Intuit built its entire small business financial ecosystem on financial data aggregation. With QuickBooks now pulling live bank feeds, payroll data, and payment processing into a single view, Section 1033 turns what was a fragile technical arrangement into a legal right — unlocking more accurate cash flow forecasting for millions of small businesses.

Affirm is spearheading the 'End of Intermediation' by evolving from a checkout tool into a vertically integrated digital bank. Following its January 2026 application for a U.S. bank charter, Affirm is moving to bypass legacy sponsor banks and card networks entirely, using Section 1033 data to replace traditional credit scores with real-time 'Cash Flow Underwriting.' By linking directly to consumer bank accounts to analyze live balances and income patterns, Affirm now bypasses the FICO-dependent ecosystem to provide instant, individualized credit at the point of sale.

Open banking is the foundational infrastructure trend. Everything else — AI-powered underwriting, embedded finance, personalized products — gets dramatically better when AI models can access complete, accurate, real-time financial data from multiple institutions simultaneously.

The Section 1033 rule effectively mandates the data infrastructure that makes every other fintech trend on this list more powerful. (For how open banking is transforming B2B payment flows specifically, see our B2B ecommerce trends for 2026.)

Stablecoins spent years in regulatory limbo. That era is ending.

In 2025 and early 2026, three things converged: the EU's Markets in Crypto-Assets Regulation (MiCA) became fully enforceable across all 27 EU member states, the US Congress advanced the GENIUS Act (Guiding and Establishing National Innovation for US Stablecoins), and major payment networks began settling real transactions in stablecoins at scale.

This isn't a cryptocurrency story. It's a payments infrastructure story.

According to the Visa Onchain Analytics Dashboard, stablecoin settlement volume on public blockchains exceeded $27 trillion in 2024 — surpassing Visa's own annual settlement volume. The growth trajectory has been exponential: from $7 trillion in 2022 to $27 trillion in two years.

PayPal launched PYUSD (PayPal USD) in August 2023 and expanded it aggressively through 2024-2025. PYUSD is now available for merchant settlements, peer-to-peer transfers, and cross-border payments across PayPal's 430 million active accounts — making it the first stablecoin backed by a mainstream payment company at consumer scale.

Visa piloted stablecoin settlement on Solana, allowing merchant acquirers to settle Visa transactions in USDC rather than traditional fiat rails. According to the same Visa Crypto research, the pilot expanded from two to six acquirer partners globally — the first time a major card network bypassed traditional correspondent banking entirely for settlement.

Circle's USDC circulation grew significantly throughout 2025, ending the year at approximately $75.3 billion, with institutional adoption driving growth. Circle's attestation reports — monthly third-party verifications of reserves — became the gold standard for stablecoin transparency that regulators now reference in proposed legislation.

The GENIUS Act — if passed — would create the first federal stablecoin licensing framework in the US, allowing non-bank issuers to obtain federal charters. This is the moment stablecoins stop being a crypto product and start being a payment rail. Banks, fintechs, and even large retailers could issue their own branded stablecoins on compliant rails. The question for 2026 isn't whether stablecoins have a role in mainstream finance. It's who controls the infrastructure.

The $1.5 trillion sitting in business checking accounts waiting to clear is, quite literally, unproductive money. Real-time payment rails are ending that — faster than most people realize.

The Federal Reserve's FedNow Service launched in July 2023 and has been expanding rapidly. As of early 2026, over 1,600 financial institutions have joined the network — including community banks and credit unions that were previously locked out of instant payment infrastructure.

On the private rail side, The Clearing House's RTP network — which operates 24/7/365 — saw instant payment transaction value surge nearly 200% year-over-year following its 2025 limit increase to $10 million, with the peak daily transaction value now exceeding $8 billion. This isn't just consumers splitting dinner checks. It's businesses paying suppliers, insurers processing claims, and gig workers receiving same-day payroll.

According to McKinsey's 2025 Global Payments Report, real-time payment transactions are growing at 15x the rate of traditional payment volume globally, with the US now catching up to markets like India (UPI) and Brazil (Pix) that have had mature instant payment infrastructure for years.

Nacha — the organization governing ACH payments — reported that same-Day ACH value reached $3.2 trillion for the full year 2024 (a 45% increase from 2023). The volume also crossed the 1 billion transaction mark for the first time in history. That milestone signals the tipping point: same-day settlement is no longer a premium feature, it's becoming the expected baseline.

Stripe integrated FedNow disbursements into its Instant Payouts product, enabling platforms to push funds to connected bank accounts in seconds — a game-changer for gig economy platforms, marketplace sellers, and insurance payouts that previously forced recipients to wait days.

JPMorgan Chase processed over $1 billion per day through instant payment rails in 2024, using real-time payments for everything from corporate treasury sweeps to consumer P2P. Their treasury management clients now expect intraday liquidity as a baseline, not a premium service.

Real-time payments are the infrastructure upgrade that makes every other fintech innovation better. AI-powered underwriting is more accurate when it can see live cash flows. Embedded finance is more valuable when disbursements are instant. Open banking is more useful when data and money move at the same speed.

The bottleneck is no longer technology — it's bank adoption. Every institution that joins FedNow in 2026 expands the network effect exponentially.

For years, the financial industry lived by a single number: 45 million 'credit invisible' Americans — they have no credit score or a file too thin to generate one.

But a landmark 2025 CFPB update revealed a different, more nuanced crisis. While only about 7 million adults are truly invisible, over 25 million are 'unscored' — meaning they have credit files that are simply too thin or stale for legacy models to read. When you add the roughly 50 million more stuck with subprime scores that don't reflect their actual creditworthiness, we aren't just looking at a data gap; we’re looking at a massive misdiagnosis of risk.

FICO was invented in 1989. It measures how you've used credit products — not whether you reliably pay your rent, manage your cash flow, maintain steady income, or keep your utility bills current. For gig workers, immigrants, young adults, and anyone who simply avoids debt, FICO actively works against them.

AI-powered alternative underwriting fixes this — by training models on cash flow data, rent payment history, utility bills, subscription payments, employment income patterns, and dozens of other signals that traditional credit bureaus ignore. This fixes the "unscored" problem by shifting the lens from past debt to current behavior.

According to Experian's alternative data research, adding cash flow data to credit models improves predictive accuracy by over 40% — meaning fewer defaults, not just wider access. This isn't a charity story. It's a risk story: lenders with better data make better decisions.

The shift toward modern data isn’t just coming from Silicon Valley — it’s coming from the industry’s bedrock. FICO is moving past its 1989 legacy with FICO Score 10T, a model that finally tracks ‘trended data’ like rent and utility history. The transition is already in motion: as of February 2026, over 40 major mortgage lenders have officially adopted 10T to responsibly expand homeownership for the ‘unscored’ and thin-file borrowers.

Experian launched Experian Boost, allowing consumers to add utility payments, streaming subscriptions, and rent payments to their credit files — resulting in an average score increase of 13 points for participants, with some thin-file consumers becoming scoreable for the first time.

Zest AI provides machine learning underwriting models to 600+ financial institutions, processing loan applications against thousands of alternative variables simultaneously. Their clients consistently report 15-20% reduction in default rates and significant expansion in approval rates for creditworthy borrowers who scored poorly on traditional models.

Nova Credit built a "Credit Passport" that translates foreign credit histories from 20+ countries into US-equivalent scores — enabling immigrants to access credit based on their verified financial history abroad rather than starting from zero. They've partnered with American Express, SoFi, and Verizon.

The Section 1033 open banking rule is the accelerant. When lenders can access real-time bank account data — with consumer permission — alternative underwriting becomes dramatically more accurate and scalable. Cash flow is the ultimate alternative data signal, and every bank will soon be legally required to share it on demand.

The FICO monopoly has had 35 years. Its replacement is being built right now.

The tokenization of real-world assets is the trend that most people in traditional finance are dramatically underestimating — and most people in crypto are dramatically overhyping. Here's the unvarnished version.

Tokenization converts ownership rights in a physical or financial asset into a digital token on a blockchain — making that ownership programmable, divisible, and tradeable on a 24/7 global market. Think: owning $500 of a commercial real estate building, receiving automatic dividend distributions, and selling your stake at 2 AM on a Sunday without a broker.

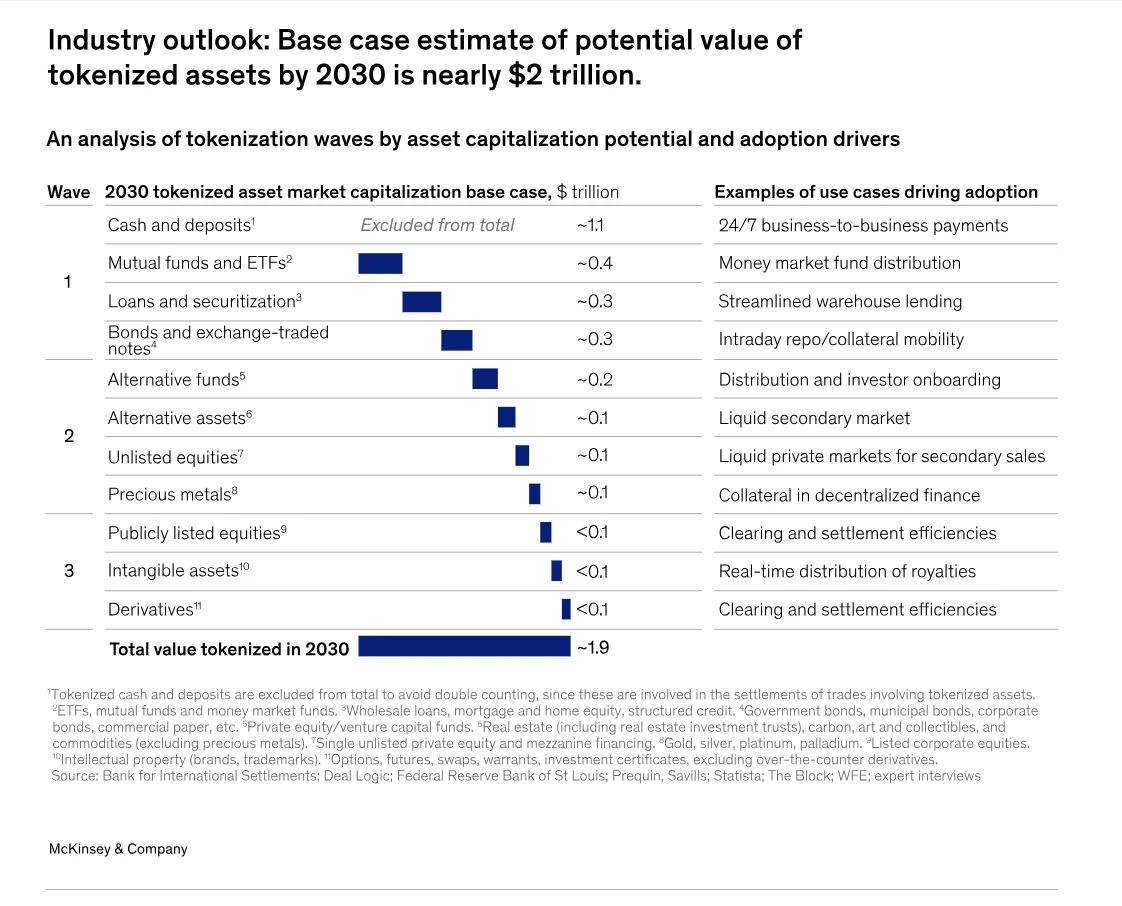

The Bank for International Settlements has analyzed tokenization extensively and identified it as one of the most significant structural changes in financial markets in decades. According to McKinsey's analysis on asset tokenization, the market for tokenized assets could reach $2 trillion by 2030 in a conservative scenario, and $16 trillion if adoption accelerates across institutional asset classes.

BlackRock launched BUIDL (BlackRock USD Institutional Digital Liquidity Fund) on Ethereum in March 2024 — a tokenized money market fund that became the largest tokenized Treasury fund within weeks of launch. As of early 2026, the fund's Assets Under Management (AUM) has surged past $2 billion, and it has distributed over $100 million in dividends to investors. It remains the dominant force in the tokenized Treasury space.

Franklin Templeton has operated its OnChain US Government Money Fund (FOBXX) since 2021 — making it one of the longest-running tokenized fund products. As of early 2026, FOBXX manages approximately $864 million in assets. Its success demonstrated that regulated fund structures can operate natively on blockchain infrastructure without sacrificing compliance.

JPMorgan's Kinexys platform (formerly Onyx) has processed over $1.5 trillion in tokenized transactions since 2020, primarily in repo markets where tokenization dramatically reduces settlement risk and collateral management overhead. Their tokenized collateral network allows institutional clients to move assets across jurisdictions in near-real-time.

The infrastructure convergence is what makes 2026 different from previous years. Regulatory frameworks for tokenized securities are clarifying in the US, EU, and Singapore simultaneously. Institutional-grade digital asset custody from BNY Mellon and State Street removes the "who holds the keys" objection.

ERC-3643, the compliance-aware token standard, gives institutions a legally defensible framework for investor whitelisting and transfer restrictions. The technical and regulatory moats are falling simultaneously — and that's when adoption curves inflect.

Somewhere in 2026, the app on your phone that processes your paycheck, stores your savings, handles your investments, covers your insurance, and lets you send money to friends is probably not a bank. And that's exactly what banks are terrified about.

The "super app" in financial services is the platform that owns your primary financial relationship — the one you open first, the one you trust with direct deposit, the one you'd miss the most if it disappeared. Right now, several very different companies are in an all-out war to become that app.

According to the same Accenture 2026 Banking Outlook, 65% of consumers are now open to using a GPT-like financial assistant offered through a digital wallet rather than a bank officer. Vericast reveals that in 2026, Only 33% of consumers feel very confident that their traditional financial institution can help them achieve their financial priorities. This lack of active value-add is what terrifies banks — the realization that they are viewed as a commodity, not a partner.

Apple has systematically assembled a financial services stack: Apple Pay (payment processing), Apple Card (credit card, currently transitioning from Goldman Sachs to JPMorgan Chase), Apple Savings (high-yield savings account, currently offering 3.65% APY), Apple Cash (P2P payments), and Tap to Pay (merchant acquiring). Apple's financial services ecosystem now touches approximately 818 million active users globally — all while Apple continues to operate without holding a single banking license.

Cash App (Block) has reached 59 million monthly active users, serving as a critical financial hub for a generation that is often unbanked or underbanked. As a primary bank for approximately 9.3 million of these users, the platform provides the full suite of banking services — including direct deposit, debit cards, stock trading, Bitcoin, and short-term lending. For a generation that never had a traditional banking relationship, Cash App is their bank.

Walmart launched One Financial, targeting its 1.6 million US employees and broader customer base with banking, early wage access, and lending products. Walmart's distribution advantage — 4,700+ US stores — gives them physical presence that digital-only challengers can't match.

The super app race is ultimately a data race. Whoever captures the most comprehensive picture of your financial behavior — spending, saving, borrowing, insuring — can offer the most personalized, most competitively priced products. Traditional banks have the data but lack the user experience.

Tech companies have the UX but lack full regulatory authorization. The middle ground — a fintech with a bank charter and tech-company design sensibility — is where the most interesting competition is happening in 2026.

Here's the dirty secret of global finance: sending $200 from the US to a family member in the Philippines still costs between 6% and 8% in fees and takes 1-5 days. That's not a technology problem. It's a network problem — a cartel of correspondent banks taking friction-rent from the world's most economically vulnerable people.

The World Bank's Remittance Prices Worldwide Database puts the global average cost of sending $200 at 6.5% as of Q1 2025 — more than three times the UN's Sustainable Development Goal target of 3%. For context, global remittance flows hit $905 billion in 2024, with $685 billion specifically going to low- and middle-income countries. This is one of the largest sources of friction in the global economy.

That friction is now being systematically removed.

Wise (formerly TransferWise) has built an internal network of local bank accounts across 80+ countries, routing transfers through local rails rather than SWIFT. Their 2025 Annual Report shows they now move £145 billion annually at an average cost of 0.52% as of 2026 — 13x cheaper than traditional wire transfers. With 15.6 million active customers, they've become the benchmark for what cross-border payments should cost.

Ripple is operating live payment corridors for financial institutions in Southeast Asia, Latin America, and the Middle East through the Ripple Payments network. Their liquidity solution — which uses XRP as a bridge currency — has processed over $100 billion in cross-border volume for financial institutions that previously relied entirely on pre-funded nostro/vostro accounts.

Stellar Development Foundation powers MoneyGram Access, allowing users to convert digital assets to local cash at MoneyGram's 470,000+ locations globally across 200+ countries. This last-mile solution bridges the gap between blockchain and the unbanked, allowing physical cash pickup without a traditional bank account. As of March 2026, the service now includes a native non-custodial wallet within the MoneyGram app, supported by a landmark SEC-CFTC ruling classifying Stellar (XLM) as a digital commodity.

The ISO 20022 messaging standard migration — completing globally through 2025-2026 — is the silent infrastructure upgrade that makes everything else possible. ISO 20022 carries vastly richer transaction data than legacy SWIFT messages, enabling AI-powered compliance screening, automated reconciliation, and real-time FX optimization that were impossible before.

Every major correspondent bank is now ISO 20022 compliant. The rails are being laid. The fee compression is coming, and it will be permanent.

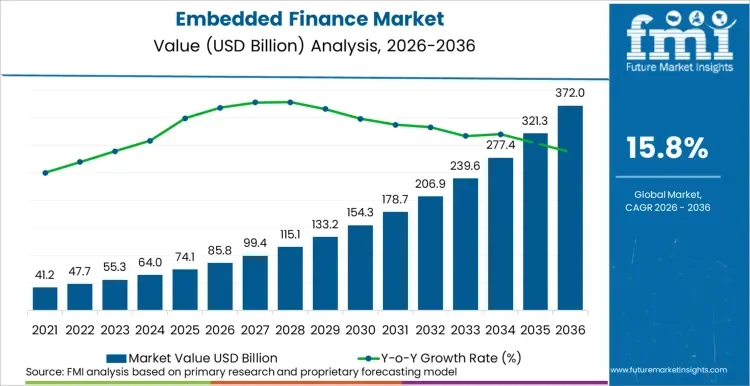

The first wave of embedded finance was "buy now, pay later at checkout." The second wave — which is where we are now — is financial services so deeply integrated into non-financial platforms that the finance becomes invisible.

Future Market Insights reports that the embedded finance market - currently valued at approximately $85.8 billion - is projected to climb to over $370 billion by 2036, growing at a CAGR of 15.8%. According to Bain & Company, in the US alone, the transaction value of embedded finance is on track to exceed $7 trillion in 2026, representing over 10% of all US financial transactions.

Here's the structural shift: by 2027, analysts project that non-financial companies in several verticals will generate more revenue from embedded financial products than from their core business. That's not a rounding error. That's a category inversion.

Shopify now offers its 3 million+ merchants a complete financial stack through Shopify Balance — a business checking account, debit card, instant payouts, and working capital loans (Shopify Capital) that underwrite based on live store revenue data, not credit scores. Merchants never need to leave the platform to manage their business finances.

Uber offers Uber Pro Card — a debit card that gives drivers instant access to their earnings after every trip, discounts on fuel and vehicle maintenance, and cash back on Uber Eats. For the 4 million US Uber drivers, it's becoming their primary financial product — issued and managed entirely by a ride-sharing company.

Amazon has embedded financial services so deeply into its ecosystem that its scale rivals major financial institutions. Amazon Pay processes nearly $100 billion annually, while its co-branded credit cards form one of the largest U.S. consumer portfolios. Rather than direct lending, Amazon Lending now operates as a high-volume marketplace, using real-time seller data to broker capital through partners like Lendistry and Affirm — effectively acting as a credit gatekeeper for millions of merchants. Yet all this has been built on top of a shopping platform.

The enabling layer for embedded finance 3.0 is Banking-as-a-Service (BaaS) infrastructure — companies like Stripe, Unit, and Synctera that let any software company embed compliant financial products in weeks. But the BaaS sector is undergoing its own consolidation after a wave of regulatory scrutiny on sponsor banks.

The companies that get embedded finance right in 2026 are the ones building on regulated, transparent BaaS providers — not the cheapest option. The cost of a compliance failure in embedded finance isn't a slap on the wrist. It's license revocation.

Look across all nine trends and one theme dominates: the infrastructure of money is being disaggregated.

For 200 years, banks had a near-total monopoly on four things: holding money, moving money, lending money, and knowing things about money. Every trend here represents a different dimension of that monopoly being dismantled.

Open banking mandates that banks share their knowledge monopoly. Real-time payment rails commoditize the movement monopoly. Stablecoins and tokenization create programmable alternatives to holding and lending. Agentic AI removes the human intermediary from the entire stack. Super apps and embedded finance capture the customer relationship before banks even enter the picture.

The irony is that none of these trends are fundamentally anti-bank. They're anti-friction. Banks that embrace them — that open their APIs, join instant payment networks, adopt AI underwriting, and build on top of tokenization rails — will come out stronger. Banks that resist them will discover that friction, when removed at scale, doesn't come back.

What this means practically: the winners in financial services over the next decade won't be defined by their balance sheet or branch network. They'll be defined by their data quality, their API surface area, and their ability to deliver financial products embedded in the moments where people actually make financial decisions — not in a branch they drive to, not in a portal they log into, but in the apps, platforms, and experiences they already live in every day.

The companies building that future aren't all in fintech. They're in retail, logistics, software, and healthcare. And that's the most disruptive thing about the fintech trends of 2026 — the most consequential ones aren't being built by fintechs at all.

Want to spot emerging fintech and business trends before they hit mainstream? Check out our guide on how to identify market trends or explore what's gaining traction on our trends dashboard.

Interested in where the money is moving next? See how Rising Trends helps you find emerging markets before they go mainstream.

Thousands of Emerging Trends

Thousands of Breakout Apps

Mega Trends

Trend Analysis Tool