Trends

The HVAC industry is in the middle of its biggest transformation in decades — and most "trends" articles barely scratch the surface. We're not talking about vague predictions here. We're talking about a full-blown refrigerant transition that's already causing supply chain chaos.

AI systems that diagnose equipment failures before they happen, heat pumps outselling gas furnaces by record margins, and a data center cooling market that's exploding because of artificial intelligence.

The global HVAC market is projected to grow from $183.9 billion in 2026 to $290.08 billion by 2034 according to Fortune Business Insights — and the companies riding these trends are the ones that'll capture that growth.

Every trend here is backed by hard numbers from the IEA, Grand View Research, MarketsandMarkets, Johnson Controls, and the companies actually building the future of heating and cooling.

The 12 HVAC trends reshaping 2026:

Let's get into it.

Here's the stat that defines the moment: in the U.S., heat pumps outsold natural gas furnaces by 32% — a record high — according to the RMI's latest global heat pump analysis. This IEA report notes that U.S. heat pump sales rose 15% overall in 2024 compared to 2023, with a 30% jump in the second half of the year.

Globally, heat pump sales rose 27% from 2020 to 2024. Europe saw a temporary dip — sales fell 21% in 2024, with Germany down nearly 50% — but early 2025 data shows signs of a strong rebound. The German Heat Pump Association (BWP) expects sales to increase by more than 30% as new incentives kick in.

The economic case is hard to argue with. Modern heat pumps reduce heating electricity use by up to 75% compared to furnaces and baseboard heaters.

Trane announced in February 2026 a new cold climate heat pump capable of performing in temperatures as low as negative 23 degrees Fahrenheit — a game-changer for northern markets that previously couldn't rely on heat pump technology. Field trials are underway across Texas, New York, Pennsylvania, Minnesota, Wisconsin, and Montana.

Carrier was the first manufacturer to make lower-GWP refrigerant heat pumps available for order, positioning itself as the early mover in the electrification-plus-refrigerant-transition double shift.

Mitsubishi Electric Trane HVAC US launched a full product line featuring R-454B for both residential and light commercial applications in April 2025, with improved cold climate heating performance, advanced sensors, and enhanced internet connectivity built in.

2026 is the year heat pumps stop being an "alternative" and become the default.

Federal tax credits, state-level rebates, and the sheer efficiency advantage are pushing adoption past the tipping point. The cold climate barrier — long the biggest objection — is falling as manufacturers like Trane push operating ranges well below zero.

The real question for 2026 isn't whether to go with a heat pump. It's which heat pump technology — air-source, ground-source, or hybrid — fits your climate and building type.

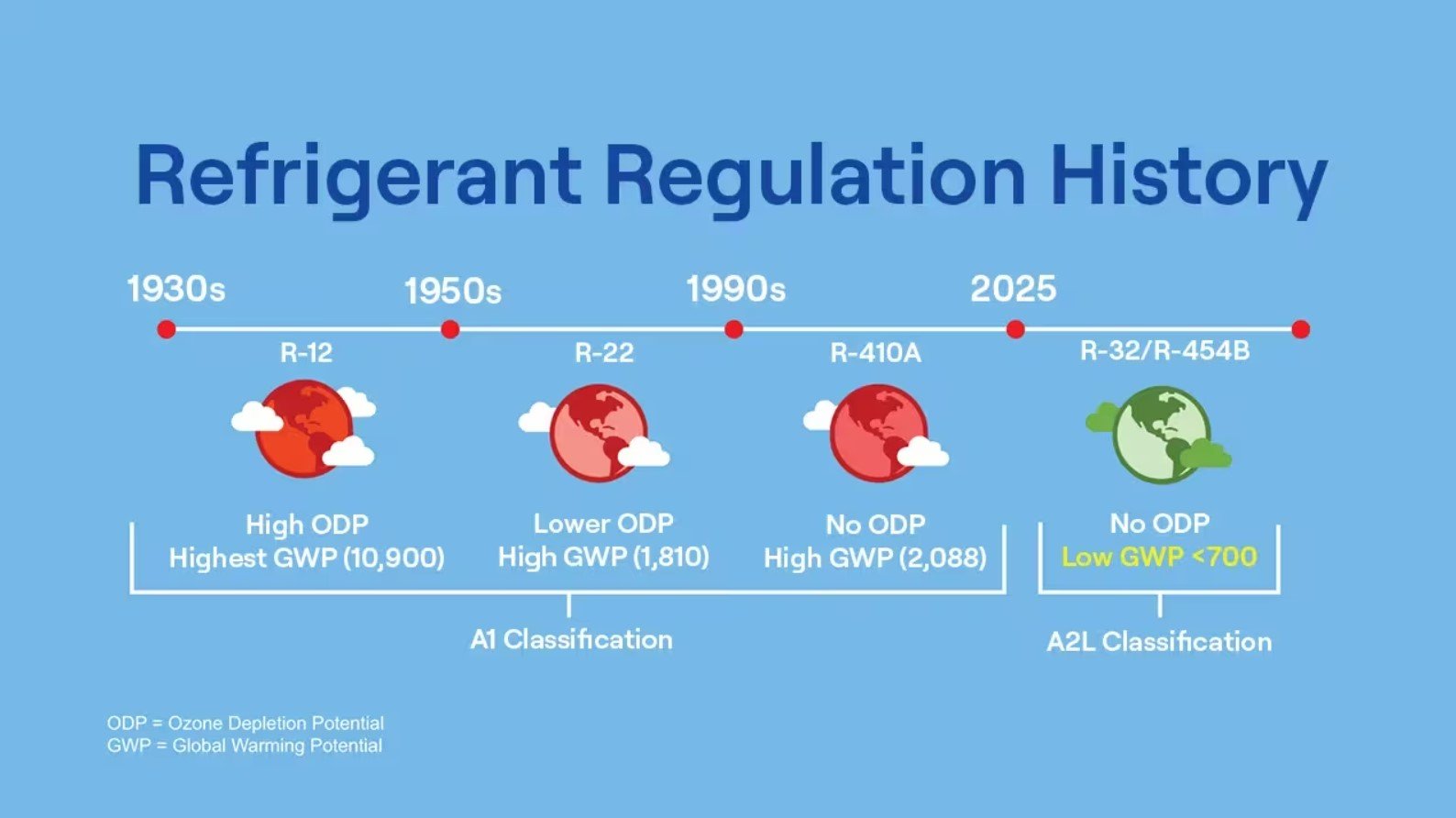

This is the most disruptive regulatory shift the HVAC industry has seen since R-410A replaced R-22.

As of January 1, 2025, manufacturing of new residential R-410A equipment ended. R-454B — with a GWP of 466, which is 78% lower than R-410A — is now the standard, according to Carrier's Puron Advance documentation.

R-454B is not a drop-in replacement. It's classified as an A2L (mildly flammable) refrigerant, requiring purpose-built equipment with built-in leak detection sensors, shut-off valves, and smart control logic.

The transition has been rocky — supply chain shortages of both R-454B refrigerant and A2L-rated cylinders have plagued the rollout.

Lennox rolled out its full R-454B product lineup — residential heat pumps, air conditioners, and the award-winning commercial Model L and Enlight families — well ahead of the 2025 deadline, using R-454B for ducted and R-32 for ductless solutions.

Carrier announced supply chain initiatives in May 2025 to increase R-454B availability without surcharges, onboarding new down packers and leveraging OEM refrigerant supply to support distribution networks.

Daikin is taking a different approach in Europe, launching a CO2-based VRF system in response to the EU's F-gas Regulation, which will phase out HFCs entirely by 2050.

The supply chain headaches will ease by mid-2026 as manufacturers scale production. But the training gap is real — technicians need certification on A2L handling, and many jurisdictions are still updating building codes for mildly flammable refrigerants.

Existing R-410A systems can still be serviced throughout their useful life, but every new installation is now R-454B territory.

For contractors, this transition is both a challenge and an opportunity. The ones who've invested in A2L training and inventory are positioning themselves ahead of competitors still scrambling to adapt.

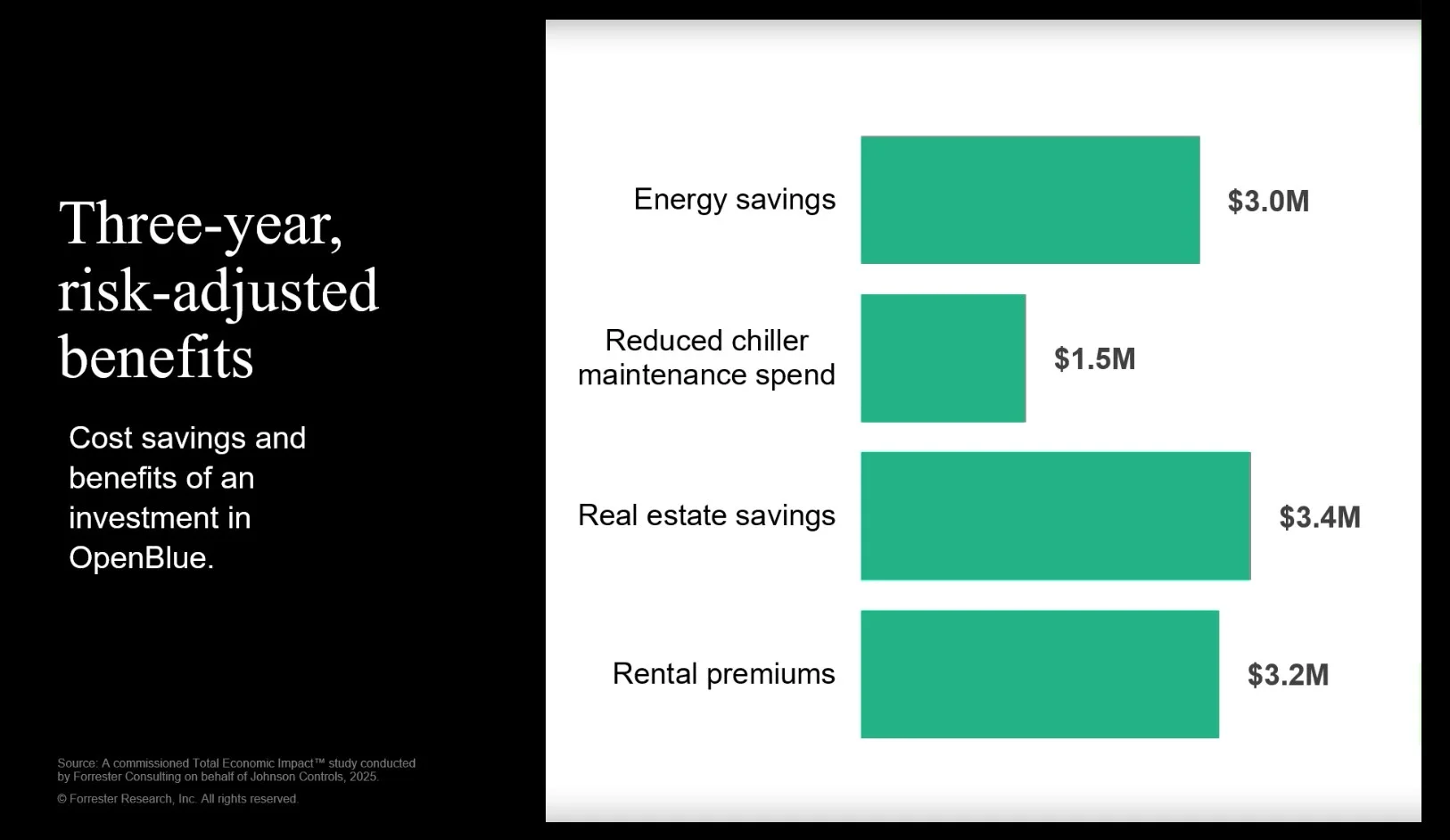

Here's a number that should get every building operator's attention: organizations deploying Johnson Controls' OpenBlue platform achieved up to 155% return on investment over three years, with up to 67% reduction in chiller maintenance — saving nearly $1.5 million over three years, according to a Forrester Total Economic Impact study commissioned by Johnson Controls.

AI-driven HVAC maintenance is shifting the entire industry from reactive "break-fix" models to proactive, data-driven strategies.

Smart sensors paired with machine learning detect inefficiencies and potential failures before they become expensive emergencies — then automatically generate service tickets.

Johnson Controls launched OpenBlue Enterprise Manager GenAI in late 2025, using autonomous agents that adjust building temperatures and lighting based on real-time grid pricing and occupancy. The platform now achieves 20-30% energy savings without human intervention — and JCI sells it as an "As-a-Service" contract.

Honeywell unveiled Connected Solutions in June 2025 — an AI-powered platform that integrates HVAC, access control, and life safety into a single interface. The AI-enabled installation process cuts deployment time from weeks or months to a matter of hours.

Siemens officially showcased Building X at AHR Expo 2026, featuring generative AI capabilities integrated into building management, with native Haystack 4 semantic tagging and secure edge-to-cloud connectivity.

By the end of 2026, AI-powered maintenance won't be a premium feature — it'll be table stakes for commercial buildings.

The convergence of cheaper IoT sensors, more powerful edge computing, and increasingly sophisticated machine learning models means even mid-size buildings can justify the investment. The shift from selling hardware to selling "outcomes-as-a-service" is restructuring the entire HVAC business model.

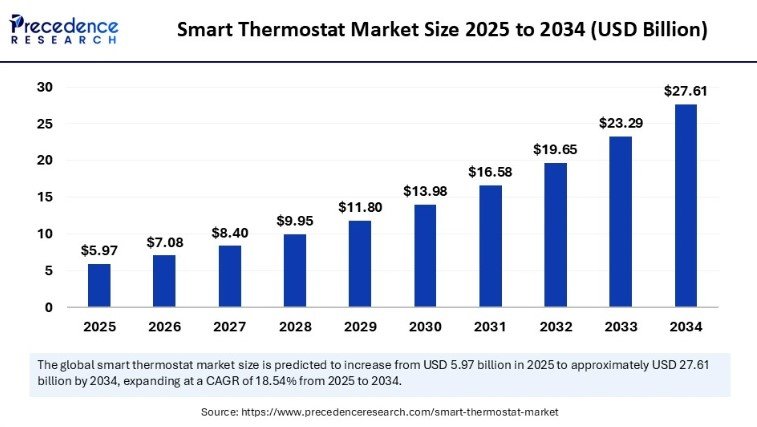

The global smart thermostat market is estimated at $7.08 billion in 2026 and is predicted to reach approximately $27.61 billion by 2034, expanding at a CAGR of 18.54%, according to Precedence Research.

That's not gradual growth — that's a market nearly quadrupling in under a decade.

Modern smart thermostats have evolved far beyond programmable schedules. They now learn occupancy patterns, integrate with home automation ecosystems, enable room-by-room zoning, and deliver real-world energy savings that justify the investment.

ecobee (now by Generac) launched the Smart Thermostat with home energy management in May 2025, and independent testing shows ecobee customers save up to 23% on heating and cooling costs — translating to savings of up to $250 per year.

Google Nest remains a market leader, with testing showing 19% energy savings over traditional programmable thermostats. The Nest Learning Thermostat's AI adapts to routines and weather patterns automatically.

Daikin's Cloud Platform analyzes weather forecasts and occupancy patterns using IoT sensors to pre-cool or pre-heat spaces, leveraging adaptive learning algorithms to reduce energy consumption by approximately 25%.

2026 is when smart thermostats graduate from "nice-to-have gadget" to "core building infrastructure." The integration with utility demand-response programs — where your thermostat adjusts automatically based on grid pricing — is turning every connected home into a node in a smarter energy grid.

Expect zoned HVAC systems paired with smart thermostats to become the standard in new construction — part of the broader smart home transformation reshaping home improvement.

The air filters market is projected to grow from $17.08 billion in 2025 to $34.66 billion by 2034, at a CAGR of 8.3%, with the HEPA segment holding the highest growth rate, according to Fortune Business Insights. And 55% of newly launched IAQ products now feature HEPA filtration, VOC monitoring, and energy-efficient designs.

Post-pandemic awareness permanently elevated IAQ expectations. But this isn't just about COVID anymore — it's about productivity, health, and regulatory compliance.

ASHRAE Standard 241 now specifically addresses infection control in building design, and state agencies are tightening filtration requirements for schools, healthcare facilities, and high-density workplaces.

Carrier has integrated advanced IAQ monitoring directly into its HVAC systems, combining real-time particulate sensing with automated ventilation adjustments — turning the air handler into a health management system.

Trane is pushing energy recovery ventilators (ERVs) as standard in new commercial installations, bringing in fresh air while retaining conditioned energy — solving the ventilation-vs-efficiency tension that plagued buildings for years.

AprilAire has expanded its whole-home IAQ product line with smart air quality monitors that integrate with HVAC systems, automatically adjusting humidity, filtration, and ventilation based on real-time sensor data.

By 2026, IAQ monitoring will be as standard as a thermostat in commercial buildings. The regulatory push is accelerating — expect codified minimum filtration efficiencies and ventilation rates for more building types.

For homeowners, whole-home IAQ systems that monitor and adjust air quality automatically are replacing standalone air purifiers as the preferred solution.

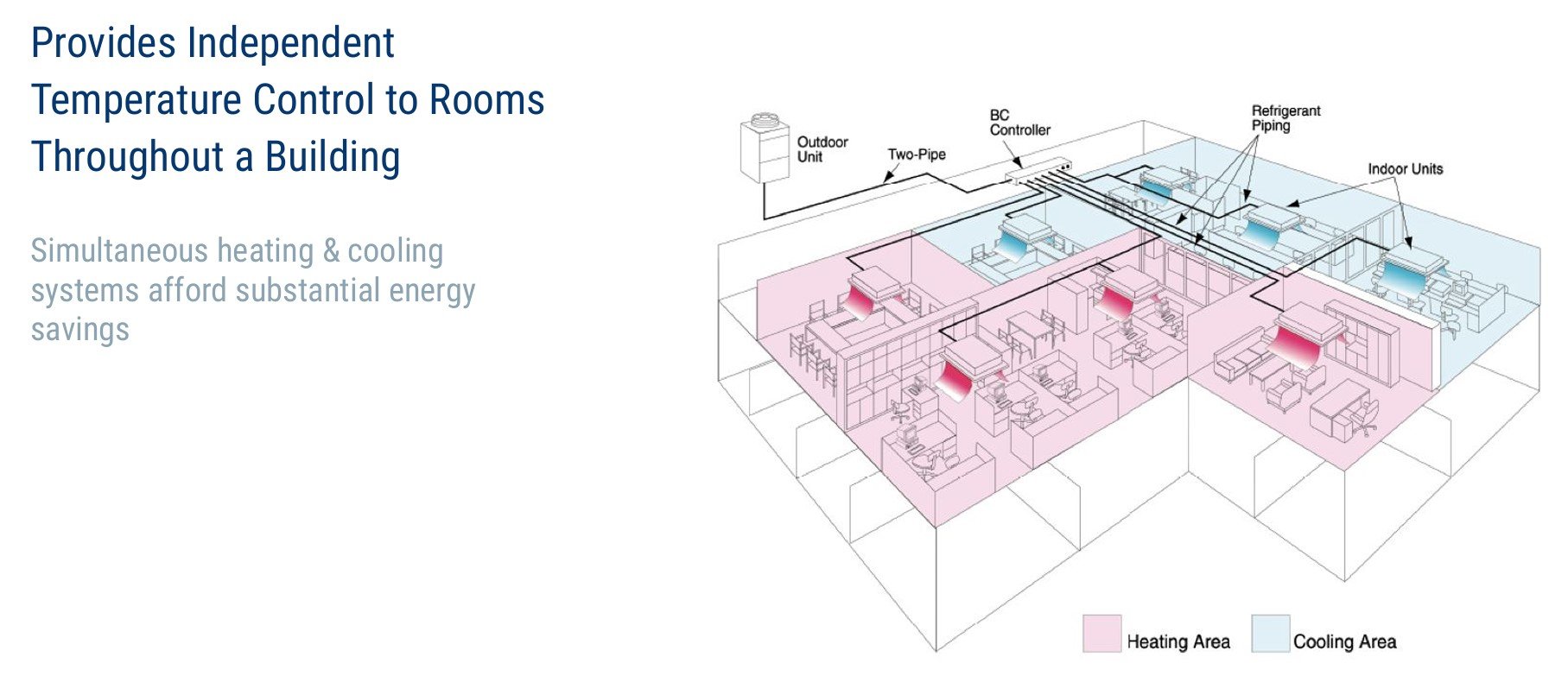

VRF systems are experiencing explosive growth. The market is expected to reach $73.88 billion by 2035, representing a CAGR of 11.3%, according to Future Market Insights.

Once limited to large commercial buildings in Asia, VRF technology is now penetrating residential, mid-size commercial, and retrofit markets worldwide.

The appeal is straightforward: VRF systems provide individual zone control, recover heat from cooling zones to use in heating zones simultaneously, and operate at partial loads far more efficiently than traditional systems. They're also quieter and eliminate the need for ductwork in many applications.

Daikin — the pioneer of VRF technology — holds 19% of the global commercial mini split market and launched a groundbreaking CO2-based VRF system for Europe in April 2025 (using the same CO2-based approach announced for the EU's F-gas phase-down), directly responding to stricter regulations.

Mitsubishi Electric updated its CITY MULTI VRF catalog for 2025-2026, with enhanced R-454B compatible models featuring advanced inverter technology and SEER ratings that push the envelope on efficiency.

LG and Samsung are competing aggressively in the U.S. VRF market, bringing price competition that's making the technology accessible for mid-size commercial projects that previously defaulted to traditional rooftop units.

VRF is the biggest structural shift in commercial HVAC design since the rooftop unit. In 2026, expect VRF to become the default specification for mid-rise commercial buildings, upscale residential, and any retrofit where ductwork installation is impractical or cost-prohibitive.

The integration of VRF with renewable energy — particularly solar — is creating near-net-zero building designs that were impossible with traditional systems.

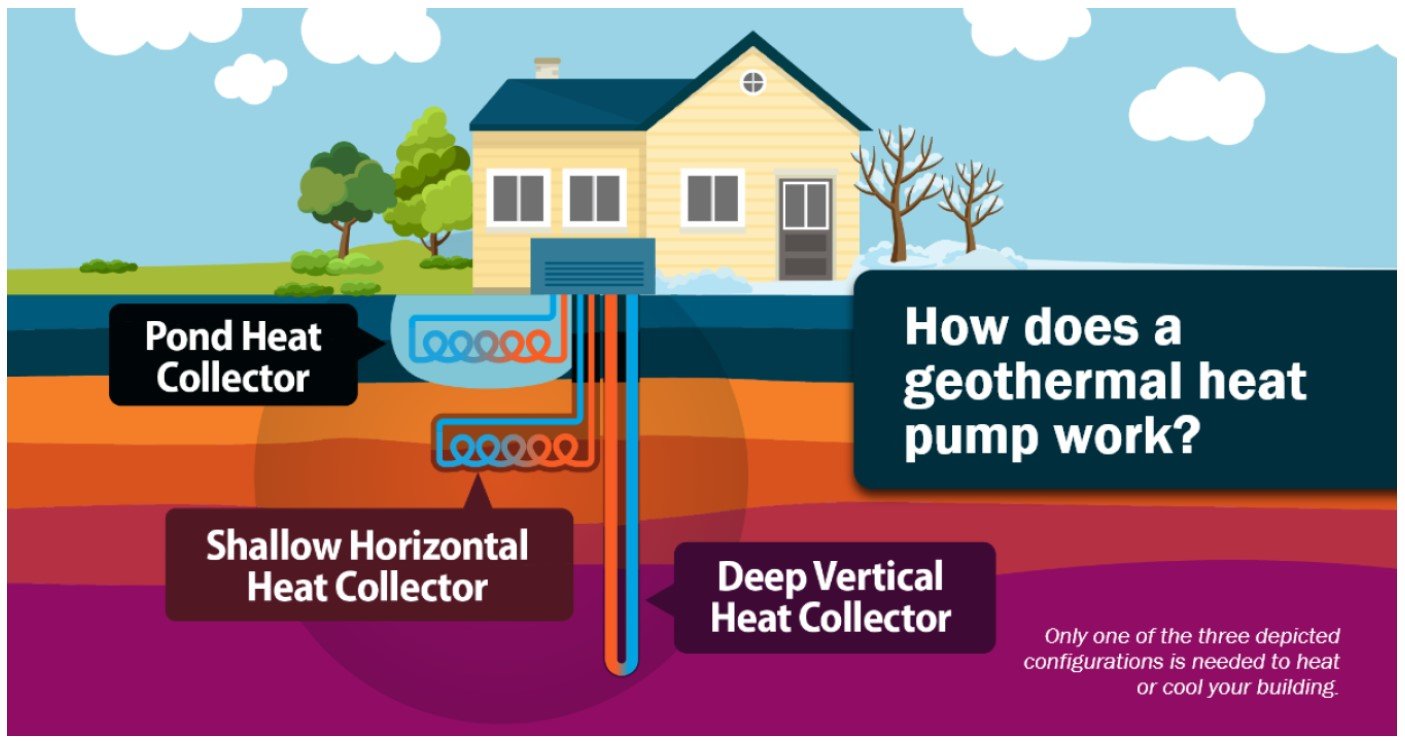

Geothermal heat pumps use stable underground temperatures to deliver heating and cooling with remarkable efficiency. ENERGY STAR-certified geothermal systems use up to 61% less energy than standard units, saving homeowners as much as $9,500 over 15 years, according to ENERGY STAR.

But here's what's actually moving the needle: the cost barrier is crumbling. Innovative financing models are making geothermal accessible to homeowners who would never have considered it before.

Dandelion Energy launched the Dandelion Geo — the highest-efficiency geothermal heat pump on the market — delivering heat at up to 5.2 COP with a proprietary heat exchanger design that avoids most main panel electrical upgrades.

Dandelion then dropped a bombshell in October 2025: the first-ever residential geothermal leasing program. Builders can integrate geothermal systems into new communities for less than traditional HVAC, and homebuyers can access geothermal for as little as $10-$40 per month. That changes the entire value proposition.

Lennar, one of the largest homebuilders in the U.S., partnered with Dandelion to install geothermal heat pumps in approximately 1,500 new homes in Colorado — proof that geothermal can scale at a builder level, not just one-off installations.

2026 is the year geothermal stops being "that expensive option the environmentalist neighbor has" and becomes a legitimate mass-market contender. The leasing model removes the upfront cost barrier — the single biggest obstacle to adoption.

As drilling technology improves and more builders integrate geothermal at the development stage, costs will continue dropping. Watch for geothermal to follow the solar adoption curve, just a few years behind.

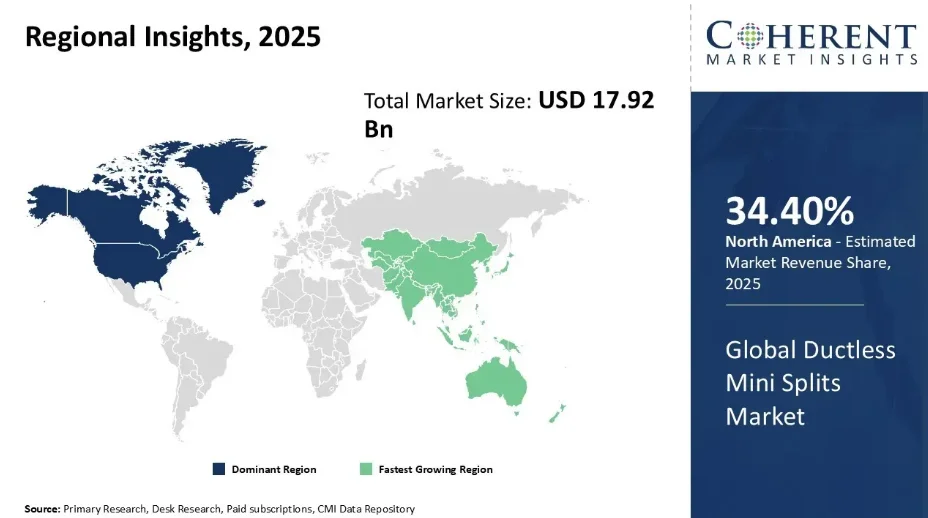

The ductless mini-split market was estimated at $17.92 billion in 2025 and is anticipated to grow to $31.31 billion by 2032 at a CAGR of 8.3%, with North America holding a 34.4% market share, according to Coherent Market Insights.

Mini-splits have evolved from a niche solution for room additions into a primary HVAC strategy for entire homes. Inverter-driven compressors deliver SEER ratings above 30, and multi-zone configurations now handle whole-home climate control without a single foot of ductwork.

Mitsubishi Electric continues to dominate the premium ductless segment, with SEER ratings pushing past 30 and new R-454B compatible models that include built-in leak detection sensors, shut-off valves, and smart control logic for A2L safety compliance.

Daikin offers single-zone ductless systems with SEER ratings up to 30.5 (ASHRAE 90.1 compliant) and has integrated AI-driven climate prediction that uses IoT sensors to anticipate heating and cooling needs based on weather forecasts.

Fujitsu and MRCOOL are driving price accessibility in the DIY market, with MRCOOL's pre-charged line sets allowing homeowners to install mini-splits without HVAC certification — a controversial but market-expanding approach.

Mini-splits are becoming the go-to solution for the enormous stock of older homes without existing ductwork — and there are millions of them.

In 2026, expect multi-zone mini-split systems to increasingly compete with traditional ducted systems even in new construction, especially in markets where energy codes push efficiency requirements beyond what most ducted systems can deliver affordably.

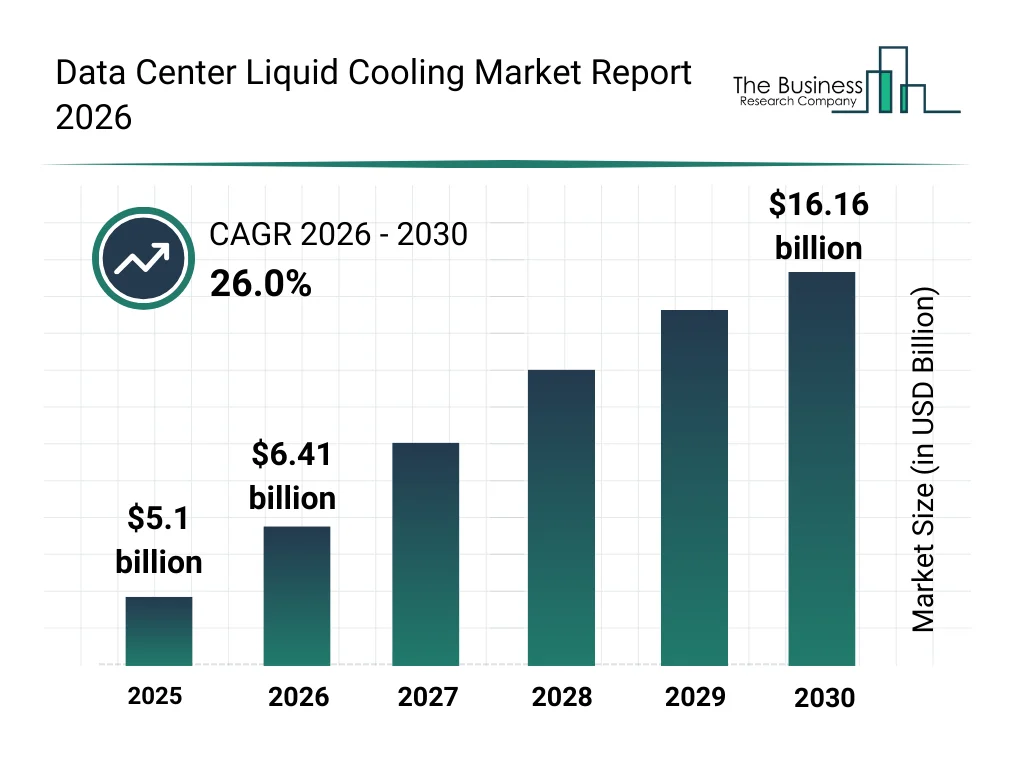

The data center liquid cooling market is anticipated to grow from $5.1 billion in 2025 to $6.41 billion in 2026 — a single-year jump of 25.7% — according to The Business Research Company. The overall data center liquid cooling market is projected to reach $16.16 billion by 2030.

This is entirely an AI story. The explosive growth of generative AI, large language models, and GPU-dense computing has created cooling demands that traditional air-based HVAC can't handle.

A single AI training rack can generate 60-100 kW of heat — five to ten times what a standard server rack produces.

Vertiv leads the data center cooling market and expanded its liquid cooling portfolio in December 2024 by acquiring assets from BiXin Energy Technology, strengthening its position in direct-to-chip and immersion cooling solutions.

Schneider Electric acquired a majority stake in Motivair Corporation in November 2024, signaling its aggressive move into high-density liquid cooling. Schneider and Vertiv are now virtually tied for global market share in data center thermal management.

Johnson Controls is positioning itself as the "thermal backbone of AI," providing precision cooling infrastructure for hyperscale data centers — where HVAC expertise meets the most demanding cooling challenge in computing history.

Data center cooling is the fastest-growing segment of the HVAC industry, full stop. In 2026, liquid cooling — including direct-to-chip, rear-door heat exchangers, and full immersion cooling — will become standard for any new AI-focused data center.

The traditional HVAC contractors who can pivot to this high-value specialization will tap into the most lucrative market in the industry.

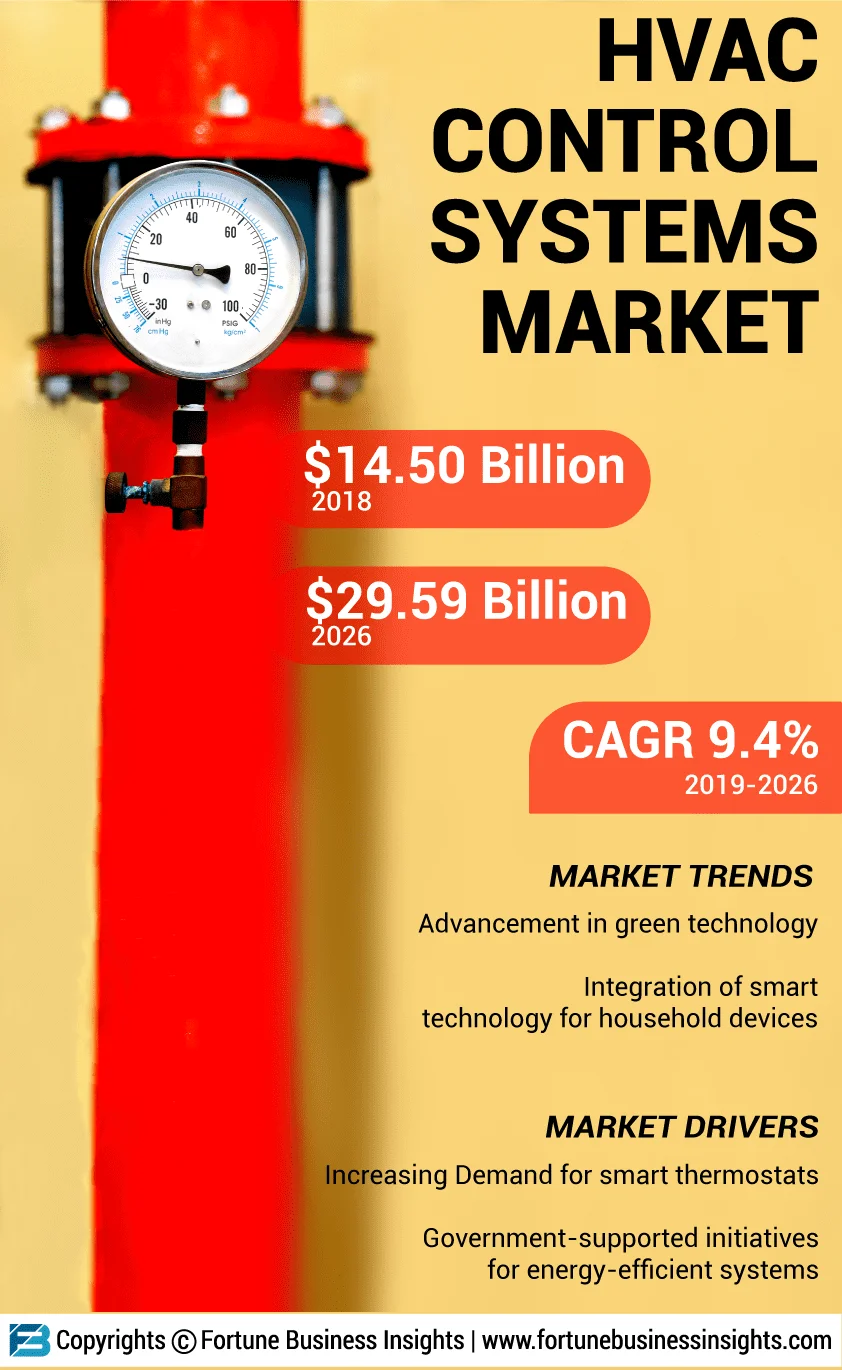

The HVAC control system market reached $29.59 billion in 2026, according to Fortune Business Insights. The days of standalone thermostats and basic building management systems are ending.

AI-powered building automation platforms now unify HVAC, lighting, security, and energy management into a single intelligent system. The shift isn't just about better technology — it's about fundamentally changing how buildings operate.

Cloud-based platforms now manage multi-building portfolios from a single dashboard, and AI-driven optimization makes decisions that human operators can't match in speed or efficiency.

Honeywell launched Connected Solutions in June 2025, integrating previously siloed systems into a single AI-powered interface. The platform's AI-enabled installation process cuts BMS deployment from weeks or months to hours — a dramatic reduction that makes smart building technology accessible to mid-size facilities.

Siemens featured its Building X platform at AHR Expo 2026, with generative AI capabilities, native Haystack 4 semantic tagging, and the Desigo CC V9 building management system that handles everything from HVAC to fire safety in a unified ecosystem.

Johnson Controls is reshaping facility management through OpenBlue's autonomous agents that adjust building systems based on real-time grid pricing, occupancy, and weather — achieving 20-30% energy savings without human intervention.

In 2026, "smart building" stops being a buzzword and becomes an operational requirement. The convergence of cheaper sensors, edge computing, and AI means that even mid-size commercial buildings can justify smart controls.

The bigger shift? Building management is moving from "monitoring and alerting" to "autonomous optimization" — systems that don't just tell you there's a problem but fix it themselves.

HVAC systems are increasingly designed to work in tandem with renewable energy. Heat pumps combined with solar installations can reduce grid reliance by up to 75% compared to fossil fuel heating, according to IEA Energy Efficiency Policy Toolkit 2025.

The integration goes both ways — grid-interactive HVAC systems can now respond to utility demand signals, turning buildings into flexible energy assets.

The math is compelling: a well-designed solar-plus-heat-pump system can approach net-zero energy costs for heating and cooling. Battery storage adds the ability to shift consumption to off-peak hours, further reducing utility bills.

Trane unveiled next-generation commercial HVAC solutions in February 2026 designed for integration with building-level renewables, including the Series R high-temperature heat pump chiller delivering hot water up to 210°F — the highest of any helical rotary screw heat pump chiller in North America.

Dandelion Energy is pairing its geothermal heat pumps with solar installations to create near-net-zero homes, combining underground thermal stability with rooftop electricity generation for a complete clean energy HVAC solution.

ecobee by Generac is uniquely positioned as both a smart thermostat and home energy management company, connecting HVAC systems with Generac's home battery and generator ecosystem to create fully integrated residential energy systems.

2026 is when HVAC and renewable energy stop being separate conversations. The proliferation of heat pumps — which run on electricity rather than gas — makes every heat pump installation a potential solar integration point.

As battery storage costs continue falling, the "solar + battery + heat pump" trifecta will become the gold standard for new residential construction in progressive markets. This aligns with the broader clean energy and sustainability trends reshaping how we build and live.

Here's the economic reality driving this trend: a full HVAC system replacement now ranges between $9,000 and $16,500, with prices nearly doubling since 2019.

What used to be a $6,000-$8,000 job is now running $12,000-$15,000 or higher, according to ServiceTitan's HVAC industry data. Combined with elevated interest rates, consumers are overwhelmingly choosing repair over replacement.

U.S. consumers spend over $10 billion annually on HVAC repair and maintenance services. According to Carrier research, only 19% of homeowners are considering installing a new system in 2026 — representing about 3.5 million units. The rest are repairing and maintaining what they have.

ServiceTitan reports that HVAC contractors are seeing the shift firsthand — maintenance agreements and service plans are becoming the primary revenue driver over equipment sales for many businesses.

BDR (Business Development Resources) is coaching HVAC contractors to adapt their business models, emphasizing service agreements, efficiency upgrades during repair visits, and financing options to bridge the gap between repair and replacement.

FTL Finance highlights that contractors offering flexible financing options are converting more repair customers into replacement customers — but the emphasis has shifted to extended payment terms that make $12,000+ investments manageable.

Every homeowner who chose a repair over a replacement is building pent-up demand that will release when conditions stabilize. Forecasters project a recovery trajectory beginning in late 2027. In the meantime, smart contractors are treating every repair visit as a relationship-building opportunity — because every aging system is a future replacement sale.

The broader implication: the HVAC industry's revenue model is diversifying from big-ticket replacements toward recurring service revenue, efficiency upgrades, and IAQ add-ons during maintenance visits.

Across all 12 of these trends, one pattern keeps emerging: the HVAC industry is transforming from a hardware business into a technology-and-services business.

Heat pumps are replacing furnaces. AI is replacing reactive maintenance. Smart thermostats are replacing programmable boxes. VRF systems are replacing ductwork. Geothermal leasing is replacing massive upfront costs. And the entire industry is moving from "sell equipment, walk away" to "manage outcomes, stay connected."

The companies winning in 2026 aren't just building better compressors or more efficient coils. They're building platforms — software ecosystems that monitor, optimize, predict, and adapt. Johnson Controls sells "As-a-Service." Honeywell deploys AI in hours instead of months. Dandelion leases geothermal for $10/month.

For homeowners, the message is clear: the HVAC system you install or upgrade in 2026 will be fundamentally more intelligent, more efficient, and more connected than anything available even three years ago. The technology has leapfrogged — and the economics, driven by federal incentives, utility rebates, and innovative financing, have never been more favorable.

For contractors and building professionals, the message is equally direct: adapt or get left behind. The technicians who understand AI diagnostics, A2L refrigerants, VRF system design, and smart building integration are the ones who'll thrive. The ones still selling boxes will struggle.

The HVAC industry isn't just heating and cooling anymore. It's energy management, air quality, building intelligence, and climate infrastructure — all wrapped into the most essential system in every building.

Want to spot emerging HVAC and building technology trends before they hit mainstream? Check out our guide on how to identify market trends or explore what's gaining traction on our trends dashboard.

Thousands of Emerging Trends

Thousands of Breakout Apps

Mega Trends

Trend Analysis Tool