Trends

Rent is getting harder to afford. Average U.S. rent has climbed 25 % since 2020, while wage growth lags. A growing group of startups promises relief through Flex Rent. For a wider look at where renter demand and housing models are heading, see our analysis of real estate trends for 2026.

Some apps report on-time splits to credit bureaus, turning rent into a credit-building tool.

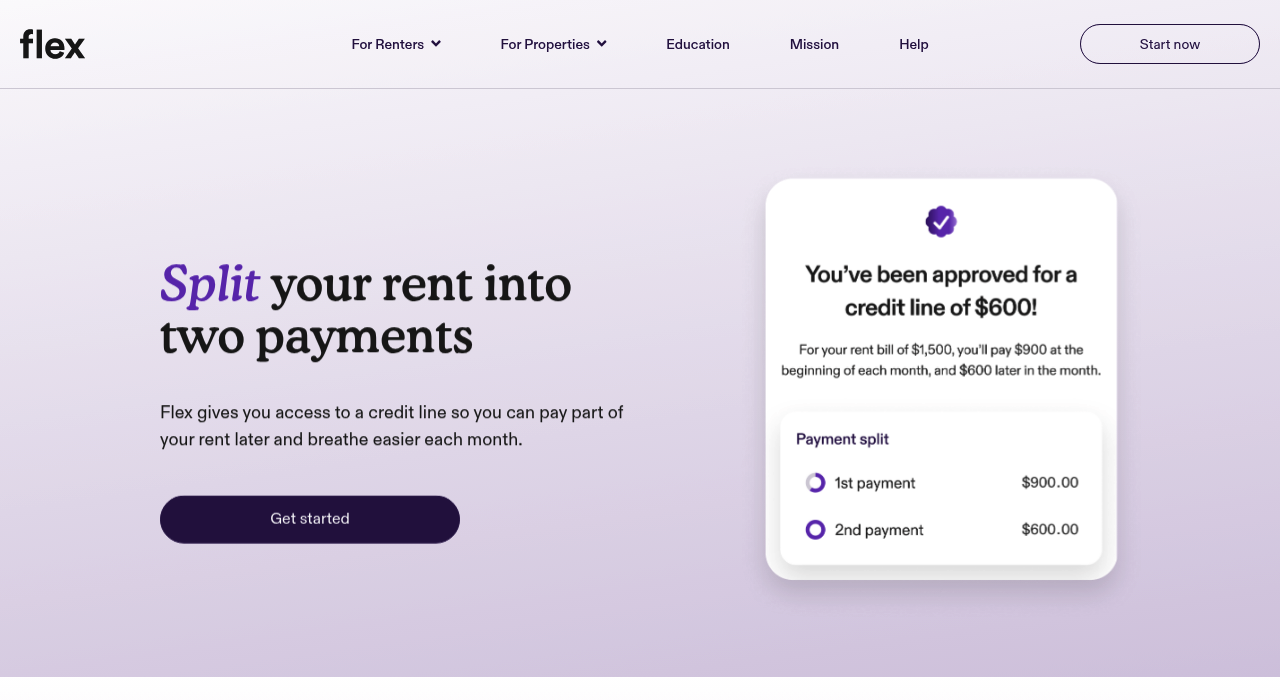

• Flex, launched in 2019, serves 200,000+ units and raised $50 M Series B led by Tiger Global, per TechCrunch.

• Livble enables U.S. renters to split monthly rent into up to four installments and just closed an acquisition by RealPage (integrating the service into its property management platform), reports The Verge.

• Property managers like Greystar now embed flexible payments in resident portals through API deals with prop-tech firms.

The U.S. has 44 million renter households. If even 5 % adopt flexible rent at an average $10 fee, annual revenue tops $264 million. Expansion to Canada, the U.K., and Australia adds millions more potential users.

Landlords

• Receive rent in full and on time.

• Lower delinquency rates can cut collection costs by up to 30 %, per a 2024 NMHC survey.

Renters

• Match payments to bi-weekly or weekly pay cycles.

• Avoid payday loans and late fees that often exceed flexible-rent charges.

• Build credit when platforms report payments.

• Bundling. Apps are adding utilities, renters insurance, and savings tools to raise revenue per user.

• Employer partnerships. Companies may offer flexible rent as a financial-wellness perk.

• AI underwriting. Real-time income and spending data could replace credit scores when approving renters.

• Policy shifts. If cities adopt “rent-smoothing” subsidies, public funds might flow through these platforms.

Paying rent once a month is a relic of the paper-check era. Flexible schedules align housing costs with modern cash flow. As fees fall and trust grows, expect Flex Rent to move from edge case to default option within the decade.

Thousands of Emerging Trends

Thousands of Breakout Apps

Mega Trends

Trend Analysis Tool